New Horizons

New Horizons

Project Management Academy

Project Management Academy

Six Sigma Online

Six Sigma Online

Velopi

Velopi

Watermark Learning

Watermark Learning

Login

Login

Project Management as a Business Investment

In this article, we will briefly look at project management as an investment and provide some suggested approaches for turning an investment in project management into big dividends.

On this page:

All businesses require investing money to get the business started, to maintain customers or clients, investing in equipment and people to run the business and to grow the business. The success of that business requires investment. Many companies only look only at the hard business assets they invest in. One of the overlooked investments is project management processes.

As a business practice, project management is an investment. It takes personnel who have the aptitude to be project managers and providing training to those people. It takes time to develop a methodology that works within the culture of the company, create policies, procedures and templates. It also takes time to ensure relevant personnel in the company buy-in to the concept that project management is a way to increase overall productivity.

Project Management as Part of Company Culture

The senior leadership of any organization must be the driving force for project management. Too often, company leaders state they want some new approach to something, to be implemented in the next month or the next quarter, yet they do not put the full weight of their position behind it. How does this manifest itself? When the leadership does not take part in the training. In reality, few senior managers are actual project managers with true project management acumen. Even fewer are certified project managers. It takes more than just an official memo to get behind a project management initiative. The mantra should be, “Make project management part of the company culture.”

To begin investing in project management, strategy sessions with key stakeholders in the organization (and maybe even hiring an outside consultant to assist) should be the first step. Using the organization’s strategic plan, develop a defined approach to implementing project management as a common business practice. It would be here that the initiative would be “chartered”. The charter is a document that outlines, at a high level: the overall goal or objective, who the key stakeholders are, what high-level risks may exist, a committed amount of funding, and so on. (If you are starting a project management initiative you might as well use project management practices to get it done!) Each organization is different, so there is not a one-size-fits-all approach to project management. Some organizations are very large and have plenty of resources, while others are small and taking time to implement project management would put a strain on production. The key factor to focus on is developing a project management initiative that works for your situation.

Invest in Training

One of the keys to any successful project management initiative is training. Depending on the current number of PMs you have, this could be an easy step, or it could take significant amounts of time and a considerable investment of capital. During the strategy meetings, determine the current level of knowledge and experience of those who will be on the front line as PMs. Ask specific questions like: Do they have education specific to project management? Are they Project Management Professional (PMP)® certification holders? What is the average number of years of experience they have? Will the people working on the technical side of the project need basic training in project management to understand and converse with the PMs? What tools will be used in managing the project and will training be needed to use those tools?

Get Leadership Buy-In

Once a defined approach is developed the next step would be to gain allies and obtain buy-in to the new initiative at all levels of the organization. Not only will they be needed to develop the processes, procedures and templates; having cheerleaders to drive the need for project management can only help. However, a word of caution is appropriate here. Choose these people wisely – choosing those who blindly follow without question or input can ultimately harm the overall goal. When choosing allies, ask questions to see if they truly understand. Questions like: What do you see as the biggest challenge to success of this initiative? Where do you think we should begin? What resources do we have to undertake this initiative? How long do you think it should take to get to a workable solution? Should we do this all at once, company-wide, or start with one or two projects? How important do you believe this initiative will be to our company growth, success, or survival?

Plan for the Project

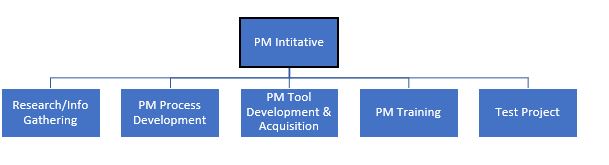

Once you have the key players selected and allies at the various levels, the next step would be to plan out how to implement the initiative. As mentioned before, each organization is different, so bear in mind that the plan used at one company may not necessarily work for another. This is where the allies you just gained will start their work. Bring as many of them together as necessary to gain input from all levels. They should develop a high-level plan for rolling this out, then work in smaller teams to develop the specifics. A high-level plan may look something like this:

As the team breaks up into smaller groups to do the detailed planning, they should consider getting other people onboard for input and suggestions. The more people allowed to participate in the initiative (at appropriate levels) the better chance of success. There’s a lot of work to do here, and as the old adage goes – two heads are better than one!

Start Small

Once the plan has been put into enough detail to implement, the next step would be to test it out on one or two smaller projects. One of the biggest mistakes an organization can make is to everything in project management all at once. The issue with this approach is simple. Not everyone will have the same level of comfort performing project management processes. If the culture of the company is one of chastising someone when they fail or make mistakes, everyone is automatically going to be afraid of making mistakes. The old saying of ‘you must first learn how to walk before you can run’, applies here. Start out with a moderately sized, small project that has minimal risk. In other words, do not attempt the first run at using project management on a project that could put the company in jeopardy. Taking baby-steps is a sounder approach to implementing a complicated initiative.

There are two methods to take a baby-step approach. First, you could take the processes, templates and procedures developed in planning and do them all on one small project. While this may seem viable, not all projects require the same processes to be used, so this method is not always successful, nor does it give the management team enough measurable feedback to make future decisions. The second method, while more successful, does take much more time. Rather than doing all process at once on a small project, select just the first few and do those, then do what you have always done. For example, if your projects in the past have never been formally chartered or no one ever developed a project management plan, then do a charter and a project management plan on the next one. Work out the kinks in the processes as you go along. Find what works and what doesn’t. Then on the next project, add a couple more processes along with the first ones you did. With each project, continue to add processes as needed and you will eventually find your teams instinctively doing project management. The best way to get the most out of your team is with a structured project workflow.

Be S-M-A-R-T

One final word about creating and investing in project management. One of the common methods is using the S-M-A-R-T approach to developing business goals and objectives. This is a fairly well know acronym that stands for Specific, Measurable, Attainable, Relevant and Timely. Of these five attributes, measurability is the most important factor. When determining the goals of the initiative, you must include measurable factors. When a business looks at the return on their investments, they use measurable factors, usually in the form of currency. However, when viewing project management as an investment, there are many factors that can be used. Reduced turnover rate, increase in productivity, a higher percentage of completed projects, fewer project terminations are just a few of the elements that can be measured.

Follow this simple approach and your investment in project management will pay-off in the long run.

Are you looking to grow your business by investing in your project managers? Check out our Business Solutions page.

Studying for the PMP Exam?

Upcoming PMP Certification Training – Live & Online Classes

| Name | Date | Place | |

| PMP Certification Training | May 20,21,22,23 8:30am-6:00pm | Columbus, OH | View Details |

| PMP Certification Training | Jul 22,23,24,25 8:30am-6:00pm | Columbus, OH | View Details |

| PMP Certification Training | Apr 29,30, May 1,2 8:30am-6:00pm | Online - Eastern Standard Time (EST) | View Details |

New Horizons

New Horizons

Project Management Academy

Project Management Academy

Velopi

Velopi

Six Sigma Online

Six Sigma Online

Watermark Learning

Watermark Learning